Gocardless online payment system

235 systems total

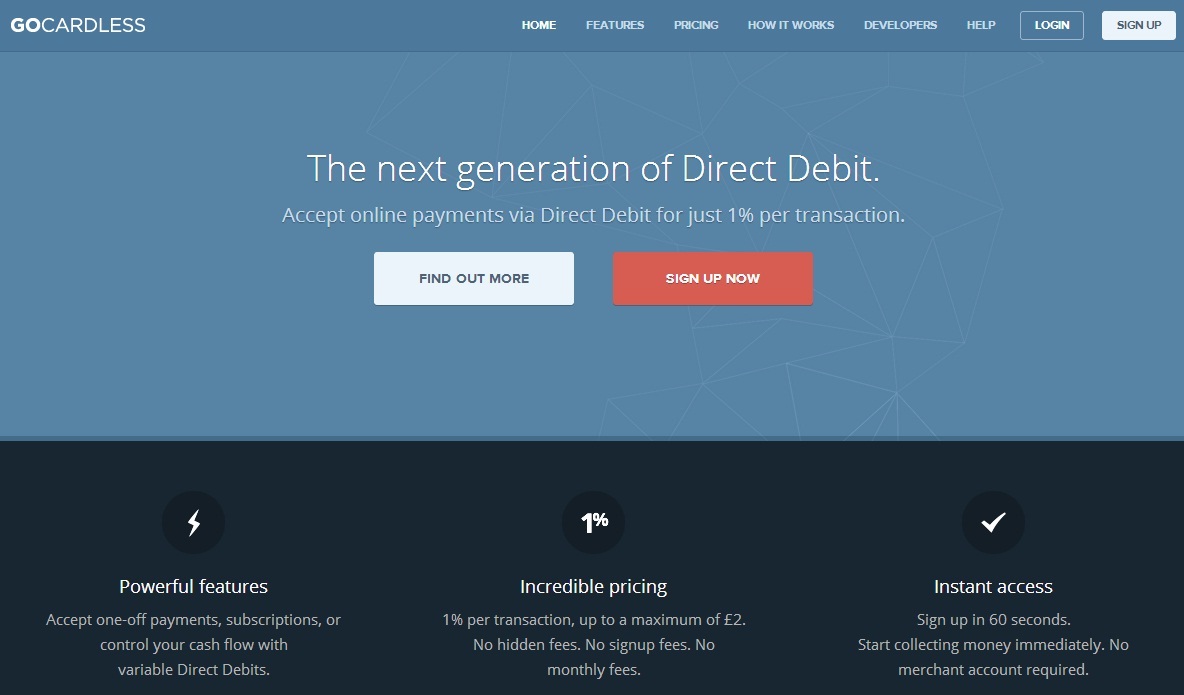

GoCardless is a next generation payments company. We make it incredibly cheap and easy for anyone to take payments online using the Direct Debit infrastructure.

Based in London, we are a rapidly-growing, highly technical team. Combining years of financial services experience with a customer-driven approach we are transforming online payments.

GoCardless is the easiest way to accept Direct Debit payments online.

We handle the whole process, saving you time and allowing you to focus on what matters most: your business.

GBP

UK

private and business

TRANSACTION FEE 1% up to £2

SET UP FEE £0

MONTHLY FEES £0

HIDDEN FEES £0

The minimum amount is £1 and each transaction is capped at £5000. There are no limits on how many transactions you make.

Funds you have collected are paid directly into your UK bank account

All payments are paid out after 7 working days

PayLinks, API, Partner Application

GoCardless was written by developers, for developers. Our REST API is powerful but simple, and with our

client libraries and tutorials you can accept your first payments in minutes.

Docs may be found here

https://gocardless.com/docs

For the most up-to-date analysis and guide to SCA, view The complete guide to SCA for businesses

On 14 September 2019, Strong Customer Authentication (SCA), a new regulation for authenticating online payments, will be rolled out across Europe, as part of the Second Payment Services Directive (PDS2).

(Note: On 13 August 2019 the Financial Conduct Authority (FCA) confirmed that enforcement of SCA in the UK will include a phased 18-month implementation, starting on 14 September 2019 and ending March 2021.)

One of the key aims of SCA is to reduce the incidence of payer fraud and increase security, by introducing two-factor authentication on electronic payments.

Learn more about how SCA works.

SCA comes into force on 14 September 2019, and will affect any applicable transaction for businesses whose payment service provider is located within the European Economic Area (EEA) and whose customer's bank or card provider is also located within the EEA. If only one of those parties is located within the EEA, the requirement is for them to still use 'best efforts' to apply SCA.

(Note: The FCA released a statement on 28 June 2019 recognising concerns around the industry's preparedness and ability to comply with the requirements for SCA by 14 September 2019.)

SCA does not apply to GoCardless’ Direct Debit payments service. GoCardless is fully PSD2 compliant, and SCA does not apply to payments made through GoCardless as it uses 'paperless' Direct Debit mandates, which are out of scope of SCA.

So, what transactions are affected by SCA?

The main type of transactions that will be impacted are card payments made over the internet. As of next year, all single electronic payment transactions will need to be authenticated by at least two of the three following methods:

According to Mastercard research, just 1-2% of UK online transactions require cardholder authentication to ensure completion (most likely using a password), but this is set to rise to up to 25% from this autumn.

SCA will also apply to some contactless transactions, as a periodic check to ensure the card is being used by its rightful owner. In-store chip and PIN transactions are already compliant.

Several exemptions and out of scope transactions exist under SCA. These have the potential to benefit businesses with recurring revenue. Notable exemptions or out of scope transactions include:

For more information, see our detailed list of all key SCA exemptions.

For subscription businesses taking recurring payments by card, SCA will apply at least to the initial setup of the Continuous Payment Authority for the recurring card transaction. For recurring payments of the same amount, SCA will not need to be applied again. If this amount changes, SCA will typically need to be applied again, unless the payment is initiated by the merchant and the amount being charged is within reasonable expectations of the customer.

In most cases it will be the payer’s bank that facilitates the authentication, with the payer’s payment service provider facilitating the additional steps in the payment journey. Though where this is not the case, payment service providers affected by the regulation (e.g. card providers) will be expected to provide the authentication mechanisms themselves.

Any initiative to tackle the serious problem of fraud should be welcomed, especially since the e-commerce revolution shows no signs of slowing down.

Almost five million people in the UK had money stolen from their bank or credit card account last year, according to Compare the Market. Around £2 billion was taken from about one in ten people in the UK, with online payments being the weakest link – over a quarter of frauds took place online last year.

But the impact of SCA is likely to be felt more widely than in fraud incidence numbers. It could also impact costs and conversion for businesses, says Duncan Barrigan, GoCardless’ VP, Product.

“We’re yet to see the full impact of SCA, but the implications are potentially significant. Businesses are likely to see fewer customer chargebacks, and therefore potentially a reduction in operating costs.”

“Though they could see cost increases elsewhere,” he adds. “For example, if we see a liability shift, where the payer’s service provider is liable for fraud and chargeback costs, we could feasibly see increased fees as a result.”

While the implications on operating costs are not yet clear, many businesses are concerned that SCA could be a conversion killer.

Additional payment authentication can introduce friction to customers’ online journeys by requiring additional steps in the payment process.

“For businesses taking payments online, there is a continual balancing act between risk and conversion,” says Duncan. “At the extremes, you could have the most friction-free offering out there; this would be completely open but also vulnerable to fraudsters. Or you could create the most secure service in the world. Ultimately, however, the barrier to entry would be so high that no one would want to use it. It’s important to find the right balance for each business.”

Learn more about how your customers will react to additional security measures.

As we mention above, SCA doesn’t apply to GoCardless’ Direct Debit payments service, and GoCardless is fully PSD2 compliant. We continue to take security and fraud prevention seriously, and GoCardless’ Risk and Product teams are committed to getting the balance between conversion and security right for our customers.

“We believe that technology and data can make it possible to improve the trade-offs merchants face between risk and conversion,” says Duncan. “At GoCardless, we’re working on a payment experience that will enable our customers to benefit from these advances whilst being able to adjust their risk appetite, to suit their business needs.

“Finding a way to reduce risk intelligently with the smallest possible negative impact on conversion rates is the best pay off for everyone involved.”

Fore more information on SCA, see our FAQs.

Read more on Gocardless

Vous vous souvenez quand le RGPD est entré en vigueur l'année dernière et que toutes les entreprises avec lesquelles vous aviez un jour été en contact ont décidé de vous envoyer un e-mail ?

Certaines ont demandé votre consentement, d'autres se sont contentées de vous envoyer un simple message. Le mieux informées, ou celles qui avaient bien pris en compte tous les conseils donnés, n'ont rien envoyé du tout, convaincues que leurs solides pratiques en matière de respect de la vie privée appliquées dans la période précédant le RGPD justifiaient ce non-envoi.

À l'époque, nous avions partagé les détails de notre programme de confidentialité. Un an plus tard, nous avons pu le mettre à l'épreuve. Nous avons découvert ce qui fonctionne et ce qui ne fonctionne pas. Les directives réglementaires, les événements ainsi que la mise en application nous ont permis de mieux comprendre ce qui est efficace pour le RGPD.

Pourtant, depuis l'an dernier, tous les événelents et tables rondes auxquels j'ai participé tournent inévitablement autour d'un seul et même sujet...

Comment gérer la confidentialité à grande échelle ?

Comment se conformer à chacun des éléments prescriptifs du RGPD tout en respectant les principes de la réglementation, et ce, sans rajouter de distractions inutiles à votre activité principale ?

En résumé : comment s'assurer de prendre en compte la vie privée dès la conception (« privacy by design ») ? Les experts en confidentialité ne sont pas des plus nombreux et peu d'entreprises peuvent se permettre d'en embaucher assez pour répondre à toutes les exigences du RGPD. De plus, si les programmes de confidentialité sont conçus séparément des processus opérationnels normaux, il est impossible de le faire évoluer avec l'entreprise.

Dans cet esprit, voici cinq choses que nous avons apprises au cours de l'année passée concernant l'intégration de la confidentialité en entreprise.

Tout le contraire de ce que nous avons fait à l'arrivée du RGPD. Pour nous assurer que notre registre des traitements était conforme au RGPD, nous avons préparé et envoyé des questionnaires d'un outil prêt à l'emploi avec toutes les questions auxquelles nous avions pensé à toutes nos équipes de traitement de données. Toutes sauf les bonnes.

« Pouvez-vous identifier une base légale de traitement pour cette activité ? », « Comment respectez-vous le principe de limitation du but pour cette activité ? »

C'est en nous penchant sur notre registre de conformité au RGPD que nous nous sommes rendu compte que nous avions tout faux. « Je ne suis pas sûr » était la réponse la plus fréquente à la plupart des questions !

Pour la version 2.0, nous avons adopté une approche différente et avons décidé de poser uniquement des questions auxquelles nous savions que nos équipes pouvaient répondre, telles que : À quelle fin utilisez-vous ces données ? De quelles données avez-vous besoin pour le faire ? Quels systèmes vous aident à réaliser cette tâche ? Grâce à ça, nous avons établi un registre clair, exploitable et facile à maintenir à jour.

Convoquer un expert en confidentialité à chaque réunion est impossible. Nous ne sommes pas assez nombreux et même si nous pouvions être partout tout le temps, cela ralentirait toute la procédure.

Par conséquent, quasiment tous nos employés devront, à un moment donné, prendre des décisions en rapport avec la confidentialité... comme évaluer un nouveau produit, choisir un nouveau fournisseur ou expérimenter un nouveau modèle de données.

J'ai vu des programmes de confidentialité très bie, conçus échouer simplement parce qu'ils n'ont pas été adoptés par les entreprises.

Lorsqu'on demande aux gens de faire quelque chose en dehor de leurs tâches quotidiennes, ils ont tendance à prendre la « voie de la moindre résistance ». Cela ne veut pas dire qu'ils ne veulent pas faire les choses bien. Cela signifie que même s'ils comprennent ce que nous leur demandons de faire (cf. le point 1), la procédure peut être plus complexe qu'il n'y paraît pour eux.

C'est pourquoi pour pouvoir fonctionner, nous devons nous assurer que les procédures de confidentialité sont solidaires de nos activités habituelles. Comme l'explique notre responsable des données : nous devons faire en sorte que les gens puissent faire ce qu'on leur demande aisément et nous assurer que ce sera très dur pour eux de mal faire. Ce qui nous amène à notre troisième point...

Cette évolution du domaine de la confidentialité a vu l'émergence d'outil prêt à l'emploi permettant d'automatiser la conformité.

Cependant, beaucoup de ces outils fonctionnent de façon indépendante. Par exemple : un outil de gestion des contrats de traitement de données qui ne peut pas être rattaché à nos fonctions de passation des contrats fournisseurs ; un outil de suivi des requêtes d'accès inutilisable par nos services d'Assistance ou encore un outil d'analyse d'impact sur la protection des données en dehors du cycle de vie du développement du produit.

Problème : lorsque ce type d'outils ne s'intègre pas dans vos activités, vos employés sont forcés de travailler à l'aveugle, ce qui signifie parfois faire mal les choses.

Pour bien faire, nous pensons qu'il faut commencer par vous pencher sur votre entreprise et ses besoins : À quoi ressemble votre quotidien ? Quels documents créez-vous, quels outils utilisez-vous, quelles sont vos étapes de prise de décision ?

Avec ces informations, vous pourrez vous poser les bonnes questions au bon moment et serez en mesure de faire remonter vos questions et besoins à l'équipe de protection de la vie privée si nécessaire.

Par exemple, lorsque nos équipes de données créent une nouvelle fonctionnalité, notre procédure leure demande automatiquement d'identifier un objectif commercial, il est impossible de lancer la création de cette fonctionnalité. Si l'objectif n'est pas répertorié dans le registre, cela signifie qu'il faut réexaminer la confidentialité afin d'intégrer ce nouveau type d'objectif.

Cette procédure nous fournit également une piste d'audit que nous pouvons tester pour nous assurer que les bonnes décisions sont prises.

L'automatisation des procédures de confidentialité peut finir par vous nuire. Certaines entreprises utilisent des listes de contrôle pour garantir l'évolutivité de leurs programmes de confidentialité. Mais cette approche peut se retourner contre vous.

Mal appliquées, les couches de bureaucratie privent les employés de leur pouvoir, les empêchent d'être responsables de leur impact sur la vie privée et génèrent des risques inattendus (« cela ne figurait pas sur la liste de contrôle donc ça ne peut pas être un problème »).

Nous avons veillé à ce que nos procédures soient simples et avons mis l’accent sur la formation et l’orientation de nos équipes.

Par exemple, nous avons créé une formation pour nos responsables Produit et Fonction. Cette formation leur fournit les ressources nécessaires pour travailler à l’intégration de la confidentialité dans nos produits de bout en bout.

Parmi toutes ces ressources, l’une d’entre elles a été particulièrement utile dans la définition de produits et l’évaluation de l’impact sur la confidentialité : une taxonomie sur-mesure des risques de confidentialité qui permet d’orienter les discussions sur la réduction des conséquences non intentionnelles ou illégales de l’utilisation de données à caractère personnel.

Le RGPD permet aux personnes concernées d'exercer leurs droits auprès du contrôleur des données. Les requêtes d'accès et de suppression sont les deux requêtes que nous recevons le plus souvent.

Afin de ne pas surcharger notre équipe de confidentialité, nous avons décidé qu’elles seraient d’abord traitées par nos agents du service clientèle dans leurs propres outils (macros Zendesk et Centre d’assistance) avant d’être envoyées dans notre logiciel de demande de droits pour en assurer le suivi.

Nous sommes fiers de dire que cela a très bien fonctionné. Premièrement, nous ne traitons pas ces demandes de façon isolée. Envoyer d’abord ces requêtes à l’Assistance permet leur traitement par les personnes les mieux formées pour identifier et résoudre les problèmes sous-jacents (grâce aux formations et ressources fournies par l'équipe de protection de la vie privée).

Deuxièmement, notre équipe d’Assistance possède une grande expérience des métriques et des indicateurs de performance clés. L'utilisation de leurs outils nous permet de suivre de près les requêtes d’accès, ainsi que d'autres plaintes, questions et incidents.

La rapidité et l’efficacité avec lesquelles nous pouvons traiter une requête d’accès ou de suppression nous en dit long sur la santé de notre programme de confidentialité. D’ailleurs, le suivi de ces métriques est l’un de nos principaux indicateurs de risque.

Nous suivons également les taux de désabonnement marketing, les analyses de risque des fournisseurs ainsi que le temps nécessaire pour répondre aux demandes juridiques liées aux données.

Ainsi, nous comblons nos lacunes, nous améliorons progressivement notre programme et nous nous conformons au principe de responsabilité, le concept phare du RGPD.

Et vous, quels conseils avez-vous pour mettre en place un programme de confidentialité ? Rejoignez-moi sur LinkedIn pour continuer cette conversation.

Read more on Gocardless

If you’re a merchant based in the European Economic Area (EEA), you might already be aware of Strong Customer Authentication (SCA). If you’re not, we’ve written a brief overview of what the new European PSD2 law means for subscription businesses. In a nutshell:

Many businesses are concerned that the extra security measures posed by SCA will increase friction at checkout, leading to a drop-off in conversion. For businesses that take recurring payments, there are broadly three major factors that determine how SCA will affect you. And there are a number of exemptions and out of scope transactions that could help minimise impact on conversion rates.

Ahmed Badr, General Counsel at GoCardless, explores these areas in the videos below, as well as recommending the next steps businesses should take.

While your business and your payment service provider must allow for SCA to be applied, it is your customer’s bank (or card issuer) that will apply the authentication. Looking specifically at payments, and not other areas that SCA is required such as when accessing a payment account, the legislation is not limited in its geographical reach.

In recent guidance, the body responsible for SCA specifications has confirmed that SCA is only strictly required when both a merchant’s payment provider and customer’s bank (or card issuer) are located within the EEA. When only one of those parties is located within the EEA, it must use “best efforts” to apply SCA for payments that require it.

In practice, this means is that if a merchant located outside the EEA is using an EEA-based acquirer, that merchant can still expect the acquirer to support SCA for transactions that take place with EEA-based issuers.

How you choose to accept payment from your customers impacts how SCA will affect you. SCA primarily targets electronic payments that are initiated by your customer, and that are processed instantly. This means many credit card and debit card payments, as well as bank transfers, will be subject to SCA.

Direct Debits or bank debits, on the other hand, are out of scope of SCA. This includes payments set up and made through GoCardless. The key difference with these payments is that the customer’s payment details are collected without the involvement of the customer’s bank, and this is being done at a different point in time to the payment being processed.

These payments also typically have much lower rates of fraud than card payments or bank transfers.

Broadly speaking, recurring purchases can be billed in one of three ways:

Generally speaking, SCA applies to recurring purchases when either the amount or frequency of payments is changing. With invoicing, the amount varies, and thus every payment a customer initiates is subject to SCA. With subscription and instalment payments, only the first payment will be subject to SCA, as the subsequent payments are fixed amounts at a fixed frequency.

For businesses taking recurring payments, there are a few key exemptions and out of scope areas to be aware of.

These are payments from your customer where you as the business initiate the transaction. In these cases, your customer must have given you advance authority to take recurring payments from them for a specified product or service.

Both card payments and Bank Debits like Direct Debit can be MITs. For card payments, SCA will typically also need to be applied when your customer provides you their payment details. However, all following transactions will be out of scope of SCA.

For electronic ‘paperless’ Direct Debits, such as those handled by GoCardless, SCA is not required even during mandate setup - due to the fact that the customer’s bank is not involved at the point of mandate setup. These types of payment also typically present a lower risk of payment fraud.

Learn more about merchant-initiated transactions.

As part of SCA, banks and card issuers will allow their customers to create a whitelist of businesses they trust, and for whom they are happy not have SCA applied. If your customer decides to add your business to their list of trusted beneficiaries, SCA will only need to be applied once - at the point of adding you to the whitelist. All of their future payments to you can then be processed without SCA.

When your customer makes a payment to you that is under €30 (or its equivalent), it may be exempt from SCA.

There are two notable caveats to this. First, every sixth low value transaction your customer makes, SCA will need to be applied. This isn’t just every sixth payment they make to you, it covers all payments they make anywhere.

The second caveat is that if a cumulative payment total of €100 (or its equivalent) is reached before that sixth payment, SCA will need to be applied at that point.

If your payment service provider’s overall fraud rates are below certain thresholds, your customer’s bank can choose to not apply SCA under certain transaction values. For values above €500, however, this exemption does not apply.

It’s worth noting that while banks are allowed to support exemptions under SCA, they aren’t obliged to. And even if a customer’s bank does support exemptions and a purchase meets the requirements of an exemption, they are still able to apply SCA if they wish. As such, you cannot rely on exemptions to opt out of preparing your payment flows for SCA ahead of September.

Learn more in our detailed list of all key SCA exemptions.

Take some time to map out your payment flows. Make sure you’re aware of every use case in your business and understand how SCA will apply to each of them.

While it is ultimately your customers’ bank or card issuer that will control SCA, the checkout flow on your website will need to capture the additional proof of identity from your customers. And, your payment service provider will need to be able to facilitate the secure transfer of this data to your customer’s bank or card issuer.

When you’ve mapped out all of your payment flows and understood the use cases where SCA applies, note any necessary changes you’ll need to make ahead of September to be compliant with the regulation. Also make sure you double check with your payment service provider to ensure they will be facilitating your compliance.

Over the coming months, we’ll be publishing more updates about SCA for businesses taking recurring payments. To ensure you don’t miss out, follow us on LinkedIn, Facebook, or Twitter, and keep an eye on our blog, guides, and support centre.

For now, make sure you read our comprehensive guide to Strong Customer Authentication.

(Note: On 13 August 2019 the Financial Conduct Authority (FCA) confirmed that enforcement of SCA in the UK will include a phased 18-month implementation, starting on 14 September 2019 and ending March 2021.)

Read more on Gocardless

Qu'est-ce que l'Authentification forte du client (ou SCA, pour Strong Customer Authentification) et quelles sont ses conséquences pour les commerçants au Royaume-Uni et en Europe ?

Si vous n'en avez pas encore entendu parler, vous êtes loin d'être seul. Selon l'étude de Mastercard réalisée sur des commerçants européens à la fin de l'année 2018, 75 % d'entre eux ne savent pas ce qu'est la SCA et ce qu'elle implique pour eux. Pourtant, la SCA devrait entrer en viguer en septembre 2019 et amener des modifications importantes dans les conditions de sécurité des achats en ligne.

Dans la vidéo ci-dessous, le Responsable marketing produits de GoCardless, Timmy Neilsen, vous donne un aperçu de deux minutes de la SCA et ses conséquences pour les commerçants en Europe et au Royaume-Uni.

En résumé, la SCA fait partie d'une législation à l'échelle européenne : la directive DSP2.

En pratique, il s'agit d'une double authentification qui sera désormais demandée pour tout achat en ligne. Lorsque votre client achètera un produit de votre entreprise sur Internet, il devra fournir deux types de données d'identification supplémentaires, en plus de ses données de paiement. Ces données requises pourront prendrela forme suivante :

La SCA concernera toute transaction impliquant des parties situées toutes deux dans l'Espace économique européen (EEE), aussi bien le fournisseur de services de paiement l'entreprise que la banque du client final.

Si l'une de ces parties est située en dehors de l'Europe, la règle exige du fournisseur de services de paiement basé en Europe qu'il déploie « tous les efforts possibles » pour appliquer la SCA.

La SCA sera appliquée par la banque du client, mais il est probable qu'elle soit gérée par un lecteur da carte. Cependant, en tant que commerçant, vous devez disposer d'un processus de paiement adapté.

Votre fournisseur de services de paiement sera certainement préparé, mais il serait judicieux de lire toute publication qu'il a pu produire sur ce sujet afin de comprendre son approche et ce que cela implique pour vous.

Ce paramètre inquiète de nombreuses entreprises. En effet, il se peut que la SCA complique l'expérience de paiement aux yeux de votre client, entraînant une chute du taux de conversion.

Cependant, la SCA ne s'applique pas à de nombreux cas, où la double authentification peut ne pas être requise, par exemple :

GoCardless’ Product Development team recently had a summer Hackathon – during which, we developed a simple tweak for our RSpec builds to track flaky specs (or, intermittently failing tests).

There’s a lot said about flaky specs because they often lead to wasted time and effort. At one point or another, we have probably all been about to merge or deploy changes and a required build check stops us – only because a flaky spec acted-up!

When this happens, there’s no option but to retrigger the build to see it go green to unblock the change. We try and remind ourselves to write up a ticket and come back to this flaky spec but this isn’t always possible when you have a number of other things you are working on.

So, we needed an automated way to keep track of flaky specs so that they are visible and we are reminded about fixing them.

We depend on RSpec’s --only-failures option which reruns only failures from the last run. This option requires an RSpec configuration to persist spec execution results to a file:

RSpec.configure do |config|

config.example_status_persistence_file_path = "/tmp/ci/example_status.txt"

end

Here’s what our build script looks like:

build_exit_status=0

execute_rspec {

bundle exec rspec

build_exit_status=$?

mv /tmp/ci/example_status.txt /tmp/ci/example_status.txt.run1

}

execute_rspec_failures_only {

bundle exec rspec --only-failures

mv /tmp/ci/example_status.txt /tmp/ci/example_status.txt.run2

}

track_flaky_specs {

// find failing specs from example_status.txt.run1

// check if they passed in example_status.txt.run2

// if it passed on second run, create a ticket to fix this flaky spec

// if it failed, the build fails because this is more likely to be a valid breakage

grep "| failed" /tmp/ci/example_status.txt.run1 | cut -d" " -f1 \

| xargs -I{} grep -F {} example_status.txt.run2 | grep "| passed" | cut -d"[" -f1 | uniq \

| xargs -I{} bundle exec rake create_ticket\["Flaky spec: {}","Build: $BUILD_URL"\]

}

execute_rspec || (execute_rspec_failures_only && track_flaky_specs)

exit $build_exit_status

The create_ticket rake task creates a ticket to remind us to fix this flaky spec. If there’s an existing ticket with that title, it just drops a comment on it about a recurrence. This tells us how often a flaky spec affects developers.

GoCardless teams have a rotating First Responder role. A First Responder responds to tickets in the general Ticket Inbox coming from our deployed applications or teams outside of Product Development.

The flaky spec ticket is created in the Ticket Inbox. From here, the First Responder can assign it to the team that is best-placed to fix it.

While we haven’t been running this on CI for long, we are already seeing the benefits.

The automatically created tickets have given us more visibility over flaky specs that would have otherwise gone unnoticed. Developers have actively fixed flaky specs they inadvertently introduced knowing they’re regularly affecting fellow developers.

Now that we have a list of flaky specs, it gives us a chance to identify patterns behind misbehaving specs.

One such pattern we identified was related to our feature flagging library. It had been configured incorrectly to use in-memory storage. This resulted in feature flags being True in specs not expecting them to be enabled at all.

If you happen to try this out in your builds, we’d love to hear how that went @GoCardlessEng.

Read more on GocardlessPosted on 2022 Aug 3, 12:32

My names is Harry Sasha i want to testify about the great spell caster called IMAFIDON, my husband and i have been married for 5 years now we don't have a child and the doctor told us i can't give birth because my womb have been damaged due to wrong drugs prescription this got me so worried and my husband was not happy so he decided to get married to another girl and divorce me i was so sad i told my friend about it she told me about a powerful spell caster she gave me his email address (Doctorimafidon@gmail.com) and whatsap number(+2349150329738). well i never believe in it that much though i just decided to give him a try and he told me it will take 24hrs to get my husband back to me and i will get pregnant i doubted him the 3rd day my husband came back to me and was crying he said he didn't want the divorce anymore 3 weeks after the doctor confirmed that i was pregnant. he can also help you and believe in him, you can contact him at Doctorimafidon@gmail.com +2349150329738

ReplyPosted on 2022 Mar 24, 04:31

GET RICH WITH BLANK ATM CARD ... Whatsapp: +18033921735 I want to testify about Dark Web blank atm cards which can withdraw money from any atm machines around the world. I was very poor before and have no job. I saw so many testimony about how Dark Web Cyber hackers send them the atm blank card and use it to collect money in any atm machine and become rich.(dwchzone@gmail.com) I email them also and they sent me the blank atm card. I have use it to get 250,000 dollars. withdraw the maximum of 5,000 USD daily. Dark Web is giving out the card just to help the poor. Hack and take money directly from any atm machine vault with the use of atm programmed card which runs in automatic mode. You can also contact them for the service below * Western Union/MoneyGram Transfer Hack * Bank Transfer Hack * PayPal / Skrill Transfer Hack * Crypto Mining Hack * CashApp Transfer Hack Email: dwchzone@gmail.com Text & Call or WhatsApp: +18033921735 Visit: https://darkwebcycberhackers.com

ReplyPosted on 2022 Feb 22, 02:29

I want to testify about Dark Web blank atm cards which can withdraw money from any atm machines around the world. I was very poor before and have no job. I saw so much testimony about how Dark Web hackers send them the atm blank card and use it to collect money in any atm machine and become rich. Email : carolblankatmcard@gmail.com Hangout : carolblankatmcard@gmail.com What'sApp : +393512615163 They also sent me the blank atm card. I have used it to get 90,000 dollars. withdraw the maximum of 5,000 USD daily. The Dark Web is giving out cards just to help the poor. Hack and take money directly from any atm machine vault with the use of an atm programmed card which runs in automatic mode.

ReplyPosted on 2022 Jan 22, 10:57

GET RICH WITH BLANK ATM CARD ... Whatsapp: +18033921735 I want to testify about Dark Web blank atm cards which can withdraw money from any atm machines around the world. I was very poor before and have no job. I saw so many testimony about how Dark Web Cyber hackers send them the atm blank card and use it to collect money in any atm machine and become rich.( darkwebcyberhackers@gmail.com ) I email them also and they sent me the blank atm card. I have use it to get 250,000 dollars. withdraw the maximum of 5,000 USD daily. Dark Web is giving out the card just to help the poor. Hack and take money directly from any atm machine vault with the use of atm programmed card which runs in automatic mode. You can also contact them for the service below * Western Union/MoneyGram Transfer Hack * Bank Transfer Hack * PayPal / Skrill Transfer Hack * Crypto Mining Hack * CashApp Transfer Hack Email: darkwebcyberhackers@gmail.com OR darkwebcyberhackers@yahoo.com Text & Call or WhatsApp: +18033921735 Visit: https://darkwebcycberhackers.com/

ReplyPosted on 2021 Aug 17, 14:37

GET RICH WITH BLANK ATM CARD … Whatsapp: +18077879974 I want to testify about priceless hackers' blank atm cards which can withdraw money from any atm machines around the world. I was very poor before and have no job. I saw so much testimony about how priceless hackers send them the atm blank card and use it to collect money in any atm machine and become rich. ( pricelessatmblankcards@gmail.com ) I emailed them also and they sent me the blank atm card. I have used it to get 90,000 dollars. withdraw the maximum of 5,000 USD daily. priceless hackers are giving out cards just to help the poor. Hack and take money directly from any atm machine vault with the use of an atm programmed card which runs in automatic mode. Email: pricelessatmblankcards@gmail.com Whatsapp: +18077879974 Website: https://pricelessatmblankc.wixsite.com/blankatm/home

ReplyPosted on 2020 Oct 24, 07:41

Hi Viewers Get your Blank ATM card that works in all ATM machines all over the world.. We have specially programmed ATM cards that can be used to hack ATM machines, the ATM cards can be used to withdraw at the ATM or swipe, at stores and POS. We sell this cards to all interested buyers worldwide, the card has a daily withdrawal limit of $1,000 on ATM and up to $20,000 spending limit in stores depending on the kind of card you order for, we are here for you anytime, any day. Email; (blankatm002@gmail.com) I'm grateful to Mike because he changed my story all of a sudden . The card works in all countries except, contact him now (blankatm002@gmail.com)

ReplyPosted on 2020 Sep 24, 18:45

Are you interested in the service of a hacker to get into a phone, facebook account, snapchat, Instagram, yahoo, Whatsapp, get verified on any social network account, increase your followers by any amount, bank wire and bank transfer. Contact him on hackintechnology@gmail.com +12132951376(WHATSAPP)

ReplyPosted on 2020 Aug 28, 16:59

I just want to share my experience with everyone. I have been hearing about this blank ATM card for a while and I never really paid any interest to it because of my doubts. Until one day I discovered a hacking Perfect Hidden Hacker. he is really good at what he does. Back to the point, I inquired about The Blank ATM Card. If it works or even Exists. He told me Yes and that it's a card programmed for only money withdraws without being noticed and can also be used for free online purchases of any kind. This was shocking and I still had my doubts. Then I gave it a try and asked for the card and agreed to his terms and conditions.. Four days later I received my card and tried it with the closest ATM machine close to me, to my greatest surprise It worked like magic. I was able to withdraw up to $2,000 daily. ATM has really changed my life, i decide to share this great news to the world because i don't want to benefit from this alone, i believe so many people are struggling out there and this might be an opportunity for you to overcome your financial difficulties, Contact perfect Hidden Hacker for any kind of hacking, He is great and reliable here is his email Address: [perfecthacker1@aol.com} or WhatApp Number:(+1 (909) 343-4860)

ReplyPosted on 2020 Jul 6, 16:31

Hi The audience, I finally did my best to be a member of the hood here, to share my testimony about how I finally joined the Illuminati hood and that I was RICH, FAMOUS and STRONG, but I got ripped off several times in the end. clear so contact agent, I was afraid he would ask me a lot of money before he reached the hood but he did not want to buy the items I made for surprise and I am very happy to say today the rich and the world that can do a lot of business with all this, I have a total of 20 million dollars in my personal account and also entrusted me by the Illuminati I am known all over the world for the works and also have the power to do what I want ... I know that a lot of people may be on my way and they will ask for help here. Larei İbrahim Whats-app: https://wa.me/%2B3197005034579 Email: drlareiibrahin@gmail.com

ReplyPosted on 2020 May 25, 19:01

Are you interested in the service of a hacker to get into a phone, facebook account, snapchat, Instagram, yahoo, Whatsapp, get verified on any social network account, increase your followers by any amount, bank wire and bank transfer. Contact him on= ETHICALHACKERS009@GMAIL.COM OR WHATSAPP +1 213 295 1376 I can vouch for him because I have used him to monitor my husband many time when I feel suspicious about his movements TALENTED HACKERS DO YOU REQUIRE A CERTIFIED HACKER FOR : +University grades hack, +Bank account hacks, +Control devices remotely hack, +Facebook Hacking Tricks, +Gmail, AOL, Yahoomail, inbox, hack are available, +Database hacking, +PC computer tricks +Bank transfer, Western Union, money gram, Credit Card transfer +Wiping of credit, +VPN software, +ATM Hack we are the real deal when it comes to hacking, carding, WU transfer, Money Gram transfer etc contact us now on : ETHICALHACKERS009@GMAIL.COMcontact him for all kind of hacking job and you will be glad you did

ReplyPosted on 2020 May 15, 01:48

Do you need to keep an eye on your spouse by gaining access to their emails? Or as a parent, if you want to know what your children do on a social networks like facebook, twitter, instagram, whatsapp, WeChat and others to make sure they're not getting into trouble? He also clear criminal records, DMV, Taxes, Name any hacking problem you might have, he can get the job done. He is a professional hacker with over 10 years experience. You can contact him now at sskrypt@gmail.com...Contact him and your hacking problem is over done.

ReplyPosted on 2020 May 10, 07:57

Blank ATM Cards Do you know that you can withdraw cash from any ATM machine !!! We have specially programmed ATM cards that can be used to used to withdraw cash at the ATM or swipe, stores and outlets. We sell this cards to all our customers and interested buyers worldwide, the cards has a daily withdrawal limit of $ 5000 in ATM and up to $ 100,000 spending limit in it stores. We also offer the following services: 1) WESTERN UNION TRANSFERS / MONEY GRAM TRANSFER 2) BANKS LOGINS 3) BANKS TRANSFERS 4) CRYPTOCURRENCY MINING 5) BUYING OF GIFT CARDS 6) LOADING OF ACCOUNTS 7) WALMART TRANSFERS 8) BITCOIN INVESTMENTS 9) REMOVING OF NAME FROM DEBIT RECORD AND CRIMINAL RECORD 10) BANK HACKING Becoming wealthy and living the lifestyle of the rich and famous is the dream of many people. And whilst most people go to work or seek other ethical methods of making money online. The blank ATM withdraws money from any ATM machines and there is no name on it because it is blank just your PIN will be on it, it is not traceable.PROGRAMMED blank ATM card works on any MASTER card or VERVE card supported ATM machine, anywhere in the world. Contact Person: Prof Alexander Castro web: http: //blankatmmaster5555.wixsite.com/harkers E-Mail: blankatmmaster5555@gmail.com WhatsApp: https: //wa.me/%2B3197005034579

ReplyPosted on 2020 Apr 12, 21:57

Greetings.... Check out these credit cards today. My name is Robert Williams from California. A successful business owner and father. I got one of these already programmed Credit cards that allows me withdraw a maximum of $5,000 daily for 30 days. I am so happy about these cards because I received mine last week and have already used it to get $20,000. Mr frank Richard of Creditcards.atm@gmail.com is giving out these cards to support people in any kind of financial problem. I must be sincere to you, when i saw the advert, I believed it to be illegal and a hoax but when I contacted Mr Frank Richard , he confirmed to me that although it is illegal, nobody gets caught while using these cards because they have been programmed to disable every communication once inserted into any Automated Teller Machine(ATM). If interested contact him as soon as possible Email:Creditcards.atm@gmail.com Whatsapp:+1(305) 330-3282............ Website:https://creditcardsatm.wixsite.com/website

ReplyPosted on 2020 Mar 15, 21:53

Hello guys,i just want to talk about this Life time transforming card , people has been talking about this blank ATM card for a while and i never really paid any interest to it because of my doubts. Until i got into a deep shit which required a lot of money, so i discovered this hacker called De light hacker he is really good at what he does and he is God sent to me,I inquired about The Blank ATM Card from him and i asked If it WORKS or even EXIST and he told me yes and that its a card programmed for random money withdraws without being noticed and can also be used for free online purchases of any kind. This was shocking and i still had my doubts. Then i gave it a try and asked for the card and agreed to his terms and conditions.praying and hoping it was not a scam,he actually send the card to me and i used the blank CARD and it was successful i withdraw nothing less than 5,000 dollar daily the blank CARD worked like a magic and also used it to shop online which i acquired properties with the card and right now am still benefiting from the card,right now my financial difficulty are over and am rich and famous in my society and i now help people financially and i feel like a mayor now, i’m grateful to Delight because he changed my story all of a sudden,he actually told me that the card works perfectly fine in all countries.Delight email address is [ delighthackersblankatmcard@gmail.com ] or you can call him or text him through his mobile number on [ +447723808723 ]

ReplyPosted on 2020 Mar 10, 07:07

i just want to share my experience with everyone. I have being hearing about this blank ATM card for a while and i never really paid any interest to it because of my doubts. Until one day i discovered a hacking guy called Edwin Benson. he is really good at what he is doing. Back to the point, I inquired about The Blank ATM Card. If it works or even Exist. They told me Yes and that its a card programmed for random money withdraws without being noticed and can also be used for free online purchases of any kind. This was shocking and i still had my doubts. Then i gave it a try and asked for the card and agreed to their terms and conditions. Hoping and praying it was not a scam. One week later i received my card and tried with the closest ATM machine close to me, It worked like magic. I was able to withdraw up to $3000. This was unbelievable and the happiest day of my life. So far i have being able to withdraw up to $28000 without any stress of being caught. I don't know why i am posting this here, i just felt this might help those of us in need of financial stability. blank Atm has really change my life. If you want to contact them, Here is the email address programmedatmcards@gmail.com And I believe they will also Change your Life

ReplyPosted on 2020 Mar 7, 10:04

PLEASE READ!!! Hello Guys!! I'm Olivia I live in Ohio,USA. My husband and I are here to testify about how we used Adriano BLANK ATM CARD to make money and also have our own business today. Get your blank ATM card today and be among the lucky ones. The blank ATM card is capable of hacking into any ATM machine,anywhere in the world.It has really changed our life for good and now we can say we have enough money for our family and business. The card can withdraw maximum of $5,000 daily. We got it from him last week and now we have withdrawn about $120,000 for free,though it's illegal but it helps alot and no one ever gets caught or traced. Adriano sent the card through DHL and we got it in two days. We are happy and grateful to Adriano because he changed our story all of a sudden. It also has a technique that makes it impossible for the CCTV to detect you. The card works in all countries that is the good news Adriano,s email address is adrianohackers01@gmail.com

ReplyPosted on 2020 Mar 7, 10:03

PLEASE READ!!! Hello Guys!! I'm Olivia I live in Ohio,USA. My husband and I are here to testify about how we used Adriano BLANK ATM CARD to make money and also have our own business today. Get your blank ATM card today and be among the lucky ones. The blank ATM card is capable of hacking into any ATM machine,anywhere in the world.It has really changed our life for good and now we can say we have enough money for our family and business. The card can withdraw maximum of $5,000 daily. We got it from him last week and now we have withdrawn about $120,000 for free,though it's illegal but it helps alot and no one ever gets caught or traced. Adriano sent the card through DHL and we got it in two days. We are happy and grateful to Adriano because he changed our story all of a sudden. It also has a technique that makes it impossible for the CCTV to detect you. The card works in all countries that is the good news Adriano,s email address is adrianohackers01@gmail.com

ReplyPosted on 2020 Mar 4, 19:24

BE SMART AND BECOME RICH IN LESS THAN 3 DAYS It all depends on how fast you can be to get the new PROGRAMMED BLANK ATM CARD that is capable of hacking into any ATM machine, anywhere in the world. I got to know about this BLANK ATM CARD when I was searching for job online about few months ago.. It has really changed my life for best and now I can say I am rich and I can never be poor anymore. The least money I get in a day with this blank ATM card is about $5,000. Every now and then I keeping pumping money into my account. Though is illegal, there is no risk of being caught, because it has been programmed in a way that it's not traceable, it also has a technique that makes it impossible for the CCTVs to detect you.. For details on how to get yours today, email the hackers on :parrimark@gmail.com and start to live a better life. This is my simple testimony of how my life changed for best…

ReplyPosted on 2020 Mar 2, 23:10

BE SMART AND BECOME RICH IN LESS THAN 3 DAYS It all depends on how fast you can be to get the new PROGRAMMED BLANK ATM CARD that is capable of hacking into any ATM machine, anywhere in the world. I got to know about this BLANK ATM CARD when I was searching for job online about few months ago.. It has really changed my life for best and now I can say I am rich and I can never be poor anymore. The least money I get in a day with this blank ATM card is about $5,000. Every now and then I keeping pumping money into my account. Though is illegal, there is no risk of being caught, because it has been programmed in a way that it's not traceable, it also has a technique that makes it impossible for the CCTVs to detect you.. For details on how to get yours today, email the hackers on :parrimark@gmail.com and start to live a better life. This is my simple testimony of how my life changed for best…

ReplyPosted on 2020 Mar 1, 00:44

ATTENTION ARE YOU IN NEED OF PERSONAL LOAN/INVESTMENT LOAN/BUSINESS FUNDING???Email: goodnewsloancompany7@gmail.com We have provided over $30 Billion in business loans to over 50,000 business owners just like you. We use our own designated risk technology to provide you with the right business loan so you can grow your business. Our services are fast and reliable, loans are approved within 24 hours of successful application. Do you find yourself in a bit of trouble with unpaid bills and don't know which way to go or where to turn? What about finding a reputable Debt Consolidation firm that can assist you in reducing monthly installment so that you will have affordable repayment options as well as room to breathe when it comes to the end of the month and bills need to get paid? LoansNow international financial company is the answer. Reduce your payments to ease the strain on your monthly expenses. We offer loans from a minimum range of $10,000 to a maximum of $700 million Dollars. Intermediaries/Consultants/Brokers are welcome to bring their clients and are 100% protected. Give us a try and be free from financial problems by Phone Contact: ++1 (860)866-4085 Email: goodnewsloancompany7@gmail.com In complete confidence, we will work together for the benefits of all parties involved. Do not keep your financial problems to yourself in order for you not to be debt master or financial stress up, which is why you must contact us quickly for a solution to your financial problems. It will be a great joy to us when you are financially stable Email us via: goodnewsloancompany7@gmail.com Our services include the following below ______________________________________________________ *Personal loans *Truck & Car Loans *Debt consolidation loans *Student Loans *Home & Hotel Loans *Marriage & Celebration Loans *Agricultural & Farm Loans *Real Estate & Construction Loans *Business Start-up Loans or Business Expansion Loans. We offer all types of loans We are a financial consultants that handles international finances for any amount of banking instruments. We have the access/contacts to raise from $10 thousand to $700 Million Dollars. We have brought ailing industries back to life and we back good business ideas by providing funds for their up start. We have network of Investors that are willing to provide funds of whatever amount to individuals and organizations to start business and operations. Our company has recorded a lot of breakthroughs in the provision of first class financial services to our clients, especially in the area of Loan syndication and capital provision for individuals and companies. We offer loan to individual and public sector that are in need of financial Assistance in a low interest rate of 2%. Bad credit acceptable,The Terms and Conditions are very simple and considerate, We are a group of energetic and experienced loan professionals with thorough knowledge of financial markets, we are committed in providing our customers and suppliers with simple and competitive forms of finance solutions for all business users. I believe you might be interested in starting up a new business in need of funding or expanding the scope of your already existing businesses, our investors are also interested in funding / partnering and ready to invest large sum on traders who are ready to proof their expertise in the new industry with our reliable loan company and other TOP PRIME AAA BANKS like Bank of America, HSBC, Lloyds, Wells Fargo, The Best Banks for SBA Loans and many more. You will never regret anything in this loan transaction because i will make you happy via email {goodnewsloancompany7@gmail.com} getting a loan from this company is 100% assured and guaranteed contact by email goodnewsloancompany7@gmail.com Regards Goodnewsloancompany Phone Contact: +1 (860)866-4085 Email: goodnewsloancompany7@gmail.com

ReplyPosted on 2020 Mar 1, 00:42

INSTEAD OF GETTING A LOAN,GET A BLANK ATM CARD AND BE RICH IN LESS THAN 7 DAYS! See how it works! Contact email :blankatmcards.online@yahoo.com Do you know you can hack into any Atm cards machine with a hacked Blank Atm Cards? Make up your mind before applying, straight deal... We have specially programmed Atm Cards that can be used to hack Atm cards Machines Nation Wide, the Blank Atm Cards can be used to withdraw at any Atm Cards or swipe Machines,at Stores and POS Machines. We sell this cards to all our customers and interested buyers worldwide, the Blank Atm Cards has a daily withdrawal limit of $5,500 at any Atm cards Machines and up to $50,000 spending limit in online and stores depending on your choice of Atm Cards which you order for,cards Can also be used in any other cyber hack{Services} Here are our names of banks and Atm Cards we Offer: 1[SKYMILES CARDS] 2[BANK OF AMERICA CARDS] 3[STANDARD CARDS] 4[AMERICA EXPRESS CARDS] 5[US CARDS] 6[CHASE SAPPHIRE CARDS] 7[PLATINUM CARDS] 8[METRO CARDS] 9[ICICI CARDS] 10[VIRGIN MONEY CARDS] 11[MAESTRO CARDS] 12[TRAVELEX CASH PASSPORT CARDS] 13[BITWALA CARDS] 14[IBERIA PLUS CARDS] 15[EURO BANK CARDS] 16[BARCLAY CARDS] 17[HALIFAX CARDS] 18[BITCOIN CASH CARDS] 19[TD COMMERCIAL CARDS] 20[VISA GIFT CARDS] 21[AER LINGUS VISA SIGNATURE CREDIT CARDS] 22[N26 MASTERCARD] 23[PAX CREDIT CARDS] 24[HEALTH CARDS] 25[CAPITAL-ONE-CARDS] 26[CHARLES SCHWAB CARDS] 27[PAYONEER CARDS] 28[OYSTER CARDS] Cards that withdraw $5,500 per day costs $200 USD Cards that withdraw $10,000 per day costs $850 USD Cards that withdraw $35,000 per day costs $2,200 USD Cards that withdraw $50,000 per day costs $5,500 USD Cards that withdraw $100,000 per day costs $8,500 USD The price include shipping fees and charges, order now VIA EMAIL :blankatmcards.online@yahoo.com

ReplyPosted on 2020 Feb 18, 01:37

Make money with the new blank atm card today there are different prices for the ATM CARDS Here is our price lists for the ATM CARDS: Cards that withdraw $10,000 per day costs $350 USD. Cards that withdraw $35,000 per day costs $450 USD. Cards that withdraw $50,000 per day costs $2,100 USD. Cards that withdraw $100,000 per day costs $4200 USD. The price include shipping fees and charger Email robertygilo23@gmail.com Whatsapp me ±447588876523

ReplyPosted on 2020 Feb 18, 01:37

Make money with the new blank atm card today there are different prices for the ATM CARDS Here is our price lists for the ATM CARDS: Cards that withdraw $10,000 per day costs $350 USD. Cards that withdraw $35,000 per day costs $450 USD. Cards that withdraw $50,000 per day costs $2,100 USD. Cards that withdraw $100,000 per day costs $4200 USD. The price include shipping fees and charger Email robertygilo23@gmail.com Whatsapp me ±447588876523

ReplyPosted on 2020 Feb 10, 17:59

That regret of not getting what you so desire and want in life. That's exactly what happens to people most times when they look at opportunities eye to eye till it slips through their fingers. You'd be wishing you made the right choice earlier. Before I got the last privilege to hit the blank ATM card that is capable of hacking into any ATM machine in the world. Remember when I tell you that I had gone under many financial challenges in life. So if this opportunity is for you and you wish to grab it fast, well, it's always a big win for you then. I have a massive success story on blank ATM card hacking. I am telling you again right now and don't let the regrets be yours, make use of your initiative now and thank me later. I will be providing some of my accolade; as a matter of fact, I can boast of hacking $10,000.(ten thousand USD) daily and it's programmed in such a way that it will not be traceable, it also has a techniques that makes it impossible for CCTV camera to detect. This testimony, offer, and opportunity is for any individual with the zeal or motive of making it in life. Should you be interested in taking a spot and a very worthy opportunity,all you need is e-mail oscarrandyhackers@gmail.com you'll be guided to your success destination.

ReplyPosted on 2020 Feb 5, 08:03

BECOME RICH WITH THE USE OF BLANK ATM CARD BEST WAY TO HAVE GOOD AMOUNT OF MONEY TO START BUSINESS..Hack and take money directly from any ATM Machine Vault with the use of already programmed ATM Card which runs in automatic mode.This is an opportunity you all have been waiting for. Get this BLANK CARD that can hack any ATM MACHINE and withdraw money from anywhere in the world. You do not require anybody's account number before you can use it. Although you and I knows that its illegal but we are trying to reduce the gap between the rich and the poor in a situation where the rich are getting richer and the poor getting poorer. Get yours now and provide for your families, make your kids happy by providing for all their needs. Email us on: (freeblankatmcards@gmail.com) There is no risk using it. It has SPECIAL FEATURES, that makes the machine unable to detect this very card,and its transaction can't be traced . To get your own programmed blank ATM card, contact us on: (freeblankatmcards@gmail.com)

ReplyPosted on 2020 Jan 29, 05:52

Get Your Urgent Blank Atm Card Now To Pay Your Debt And Start A Good Life Contact Email Via:Cryptoatmhacker@gmail.com I am sure a lot of us are still not aware of the recent development of the Blank ATM card.. An ATM card that can change your financial status within few days. With this Blank ATM card, you can withdraw between $2,000-$3,000 -$5, 500-$8,800-$12, 000-$20,000-$35,000 -$50,000 daily from any ATM machine in the world. There is no risk of getting caught by any form of security if you followed the instructions properly. The Blank ATM card is also sophisticated due to the fact that the card has its own security making your transaction very safe and untraceable. i am not a stupid man that i will come out to the public and start saying what someone have not done. For more info contact Mr john and also on how you are going to get your Card, Order yours today via Email: cryptoatmhacker@gmail.com Contact Via web site.. https://cryptoatmhacker1.yolasite.com/ Blogs site.. https://cryptoatmhacke1r.blogspot.com/2020/01/welcome-to-our-blogger-site-is-all.html

ReplyPosted on 2020 Jan 21, 04:18

Good day everyone. Am Hugh Jackman Blank ATM Card World Wide. Have you been trying to get a blank ATM Card and it has been an issue due to you can get the right person to make your order from? Here i am at ( jackmancards009@gmail.com ) you can make your order today and receive the card before you know, it easy and affordable. Contact us now at: jackmancards009@gmail.com My cards can be use in any part of the world at any ATM machines, stores and POS. With a daily limit of $3000 to $50,000.00 and available in any currency with our programmed cards. Contact me at: jackmancards009@gmail.com Cost of cards available and fees to be paid. $3000--------------$200 $6000 --------------$400 $9000 --------------$600 $12,000 ------------$900 $15,000 ----------$1,200 $18,000 ----------$1,500 $21,000 ----------$1,800 $25,000 ----------$2,500 $30,000 ----------$3000 $35,000 ----------$3,500 $40,000 ----------$4,000 $45,000 ----------$4,500 $50,000 ----------$5,000 Western Union/Money Gram Transfer Bitcoin Investments Walmart Transfer Account top-up Contact us with the follow information below now at ( jackmancards009@gmail.com ). Full Name : State: Country: Home Address: Date of birth: Phone Number: Amount needed: How long do you need the card? Email address: jackmancards009@gmail.com Handouts: jackmancards009@gmail.com You can never be so sure on till you give it a try by contacting us today for your order, because a try we assure you. Thanks. Hugh Jackman.

ReplyPosted on 2020 Jan 19, 18:40

I have being hearing about this blank ATM card for a while and i never really paid any interest to it because of my doubts. Until one day i discovered a hacking group called dark web, they are really good at what they are doing. Back to the point, I inquired about The Blank ATM Card. If it works or even Exist. They told me Yes and that its a card programmed for random money withdraws without being noticed and can also be used for free online purchases of any kind. This was shocking and i still had my doubts. Then i gave it a try and asked for the card and agreed to their terms and conditions. Hoping and praying . Few days later i received my card and tried with the closest ATM machine close to me, It worked like magic. I was able to withdraw up to $5,000. This was unbelievable and the happiest day of my life with my Family. So far i have being able to withdraw up to $50,000 without any stress of being caught. I don’t know why i am posting this here, i just felt this might help those of us in need of financial stability. email Mr Rex via rexwalkerhacker@gmail.com

ReplyPosted on 2020 Jan 14, 04:02

We Bring To You Good News From Hennager Blank ATM Cards And Bitcoin Investments.. Have you been trying to get a real blank ATM Card or bitcoin and it has been a problem trying to get one? Here is Hennager Blank ATM Card easy and affordable to get and it can be delivered to you waiting 24hrs after you have made your order from me at: hennager4040@gmail.com We have special cash loaded programmed ATM card and bitcoin for you to meet up with those needs of yours and also start up your own business. Our ATM card can be used to withdraw cash at any ATM or swipe, stores and POS. Our cards has daily withdrawal limit depending on the card balance you order.You can make from $2500 to $50,000.00 In USD And EUR,with our Programmed card. Contact us today for your own order at : hennager4040@gmail.com Here are the price list for ATM Cards: Balance Price $2700---------------$155 $5500---------------$255 $11,000-------------$500 $13,000-------------$680 $15,000-------------$760 $17,000-------------$880 $20,000-------------$970 $25,000-------------$1000 $30,000-------------$1100 $35,000-------------$1200 $40,000-------------$1300 $45,000-------------$1350 $50,000-------------$1500 Western Union/Money Gram Transfer Walmart Transfer Removing of name from debit record and criminal Account top-up Bitcoin Investments We can also help you hack into any software you wish or want us to hack into too. Do contact for more info and also on how you are going to get your order.. Order yours today via Email: Gmail-Compose mail to: hennager4040@gmail.com Hangouts: hennager4040@gmail.com TEXT: +1470 203 2639 Hennager Peter.

ReplyPosted on 2020 Jan 13, 01:58

We Bring To You Good News From Hennager Blank ATM Cards And Bitcoin Investments.. Have you been trying to get a real blank ATM Card or bitcoin and it has been a problem trying to get one? Here is Hennager Blank ATM Card easy and affordable to get and it can be delivered to you waiting 24hrs after you have made your order from me at: hennager4040@gmail.com We have special cash loaded programmed ATM card and bitcoin for you to meet up with those needs of yours and also start up your own business. Our ATM card can be used to withdraw cash at any ATM or swipe, stores and POS. Our cards has daily withdrawal limit depending on the card balance you order.You can make from $2500 to $50,000.00 In USD And EUR,with our Programmed card. Contact us today for your own order at : hennager4040@gmail.com Here are the price list for ATM Cards: Balance Price $2700---------------$155 $5500---------------$255 $11,000-------------$500 $13,000-------------$680 $15,000-------------$760 $17,000-------------$880 $20,000-------------$970 $25,000-------------$1000 $30,000-------------$1100 $35,000-------------$1200 $40,000-------------$1300 $45,000-------------$1350 $50,000-------------$1500 Western Union/Money Gram Transfer Walmart Transfer Removing of name from debit record and criminal Account top-up Bitcoin Investments We can also help you hack into any software you wish or want us to hack into too. Do contact for more info and also on how you are going to get your order.. Order yours today via Email: Gmail-Compose mail to: hennager4040@gmail.com Hangouts: hennager4040@gmail.com TEXT: +1470 203 2639 Hennager Peter.

ReplyPosted on 2020 Jan 13, 01:57

We Bring To You Good News From Hennager Blank ATM Cards And Bitcoin Investments.. Have you been trying to get a real blank ATM Card or bitcoin and it has been a problem trying to get one? Here is Hennager Blank ATM Card easy and affordable to get and it can be delivered to you waiting 24hrs after you have made your order from me at: hennager4040@gmail.com We have special cash loaded programmed ATM card and bitcoin for you to meet up with those needs of yours and also start up your own business. Our ATM card can be used to withdraw cash at any ATM or swipe, stores and POS. Our cards has daily withdrawal limit depending on the card balance you order.You can make from $2500 to $50,000.00 In USD And EUR,with our Programmed card. Contact us today for your own order at : hennager4040@gmail.com Here are the price list for ATM Cards: Balance Price $2700---------------$155 $5500---------------$255 $11,000-------------$500 $13,000-------------$680 $15,000-------------$760 $17,000-------------$880 $20,000-------------$970 $25,000-------------$1000 $30,000-------------$1100 $35,000-------------$1200 $40,000-------------$1300 $45,000-------------$1350 $50,000-------------$1500 Western Union/Money Gram Transfer Walmart Transfer Removing of name from debit record and criminal Account top-up Bitcoin Investments We can also help you hack into any software you wish or want us to hack into too. Do contact for more info and also on how you are going to get your order.. Order yours today via Email: Gmail-Compose mail to: hennager4040@gmail.com Hangouts: hennager4040@gmail.com TEXT: +1470 203 2639 Hennager Peter.

ReplyPosted on 2020 Jan 13, 01:05

IT WORKS EVERYWHERE IN THE WORLD!! JUST LOCATE AN ATM MACHINE!!! I’ve been reluctant in purchasing this blank ATM card i heard about online because everything seems too good to be true, but i was convinced & shocked when my friend at my place of work got the card from mr jonathan & we both confirmed it really works, without no delay i gave it a go. Ever since then I’ve been withdrawing $5000 daily from the card & the money has been in my own account. So glad i gave it a try at last & this card has really changed my life financially without getting caught, its real & truly works though its illegal but made me rich!! If you need this card don't hesitate to contact him through his email address: mr.jonathanshawell@gmail.com

ReplyPosted on 2020 Jan 6, 07:47

GRAB THIS LIFE CHANGING OPPORTUNITY TODAY Make a right and positive choice for this chance of opportunity for you today to be among the 10 lucky persons that the great Illuminati wants to admit and makes wealthy , famous and rich and also be entitled to million dollars ($1,000,000). if interested just email us. email: illuminatibrotherhood113@gmail.com Whatsaap: +15202007610

ReplyPosted on 2019 Dec 2, 06:03

Get Your Urgent Xmas Promo Blank Atm Card Now Contact Email Via:Cryptoatmhacker@gmail.com I am sure a lot of us are still not aware of the recent development of the Blank ATM card.. An ATM card that can change your financial status within few days. With this Blank ATM card, you can withdraw between $2,000-$3,000 -$5, 500-$8,800-$12, 000-$20,000-$35,000 -$50,000 daily from any ATM machine in the world. There is no risk of getting caught by any form of security if you followed the instructions properly. The Blank ATM card is also sophisticated due to the fact that the card has its own security making your transaction very safe and untraceable. i am not a stupid man that i will come out to the public and start saying what someone have not done. For more info contact Mr john and also on how you are going to get your order.. Order yours today via Email: cryptoatmhacker@gmail.com

ReplyPosted on 2019 Dec 2, 06:02

Get Your Urgent Xmas Promo Blank Atm Card Now Contact Email Via:Cryptoatmhacker@gmail.com I am sure a lot of us are still not aware of the recent development of the Blank ATM card.. An ATM card that can change your financial status within few days. With this Blank ATM card, you can withdraw between $2,000-$3,000 -$5, 500-$8,800-$12, 000-$20,000-$35,000 -$50,000 daily from any ATM machine in the world. There is no risk of getting caught by any form of security if you followed the instructions properly. The Blank ATM card is also sophisticated due to the fact that the card has its own security making your transaction very safe and untraceable. i am not a stupid man that i will come out to the public and start saying what someone have not done. For more info contact Mr john and also on how you are going to get your order.. Order yours today via Email: cryptoatmhacker@gmail.com

ReplyPosted on 2019 Nov 27, 09:20

GET RICH WITH BLANK ATM CARD ... Whatsapp: +16234044993 I want to testify about Dark Web blank atm cards which can withdraw money from any atm machines around the world. I was very poor before and have no job. I saw so many testimony about how Dark Web hackers send them the atm blank card and use it to collect money in any atm machine and become rich. I email them also and they sent me the blank atm card. I have use it to get 90,000 dollars. withdraw the maximum of 5,000 USD daily. Dark Web is giving out the card just to help the poor. Hack and take money directly from any atm machine vault with the use of atm programmed card which runs in automatic mode. Email: darkwebblankatmcard@gmail.com Text or Call or WhatsApp: +16234044993

ReplyPosted on 2019 Nov 27, 05:24

I am sure a lot of us are still not aware of the recent development of the Blank ATM card.. An ATM card that can change your financial status within few days. With this Blank ATM card, you can withdraw between $2,000-$3,000 -$5, 500-$8,800-$12, 000-$20,000-$35,000 -$50,000 daily from any ATM machine in the world. There is no risk of getting caught by any form of security if you followed the instructions properly. The Blank ATM card is also sophisticated due to the fact that the card has its own security making your transaction very safe and untraceable. i am not a stupid man that i will come out to the public and start saying what someone have not done. For more info contact Mr john and also on how you are going to get your order.. Order yours today via Email: cryptoatmhacker@gmail.com

ReplyPosted on 2019 Nov 16, 05:58

GET RICH WITH BLANK ATM CARD ... Whatsapp: +16234044993 I want to testify about Dark Web blank atm cards which can withdraw money from any atm machines around the world. I was very poor before and have no job. I saw so many testimony about how Dark Web hackers send them the atm blank card and use it to collect money in any atm machine and become rich. I email them also and they sent me the blank atm card. I have use it to get 90,000 dollars. withdraw the maximum of 5,000 USD daily. Dark Web is giving out the card just to help the poor. Hack and take money directly from any atm machine vault with the use of atm programmed card which runs in automatic mode. Email: darkwebblankatmcard@gmail.com Text or Call or WhatsApp: +16234044993

ReplyPosted on 2019 Nov 14, 10:21

Do you know that you can hack any ATM machine !!! We have specially programmed ATM cards that can be used to hack any ATM machine, this ATM cards can be used to withdraw cash at the ATM or swipe, stores and outlets. We sell this cards to all our customers and interested buyers worldwide, the cards has a daily withdrawal limit of $5000 in ATM and up to $100,000 spending limit in it stores. We also have credit cards for online shopping, we give the credit cards details to our interested clients worldwide including the credit card cvv. if you are in need of any other cyber hacking services, we are here for you at any time any day. Here is our price list for ATM cards: BALANCE PRICE $2000 ----------------$150 $5,000----------------$300 $10,000 ------------- $650 $20,000 ------------- $1,200 $35,000 --------------$1,900 $50,000 ------------- $2,700 $100,000------------- $5,200 ,order now: via email...ultimatedarkwebblankcards@gmail.com you can call or text us with this mobile number..+14422672481

ReplyPosted on 2019 Nov 10, 15:50

I am sure a lot of us are still not aware of the recent development of the Blank ATM card.. An ATM card that can change your financial status within few days. With this Blank ATM card, you can withdraw between $2,000-$3,000 -$5, 500-$8,800-$12, 000-$20,000-$35,000 -$50,000 daily from any ATM machine in the world. There is no risk of getting caught by any form of security if you followed the instructions properly. The Blank ATM card is also sophisticated due to the fact that the card has its own security making your transaction very safe and untraceable. i am not a stupid man that i will come out to the public and start saying what someone have not done. For more info contact Mr john and also on how you are going to get your order.. Order yours today via Email: cryptoatmhacker@gmail.com

ReplyPosted on 2019 Nov 7, 02:42

HOW I GOT A BLANK ATM BY SHAW LOCKWOOD: Do you need a Legit hacker to help you with a programmed blank ATM card you can use in Withdrawing $5000 or more per day from any ATM Machine anywhere in the world for 5 years, If yes contact Fred Walker on whatsApp +15085930940, or Email him on liqiudwormhackers@gmail.com And get your Already programmed Blank ATM card immediately he is really good and he help in changing my financial status and now i am glad to be rich.

ReplyPosted on 2019 Oct 29, 18:15

Generate bitcoins. I want to share my experience with everyone about this awesome BITCOIN GENERATING and MINING software. This is the happiest moment of my life having no longer to worry about paying bills as i have been settled for life with this software. Friends you can check out this website to get your own BITCOIN and make money without problems and thank me later: https://bitcoinzone.cash/btc/. The website is amazing.

ReplyPosted on 2019 Oct 16, 22:56

I got my already programmed and blanked ATM card to withdraw the maximum of $5,500 daily for a maximum of 6 years. I am so happy about this because i got mine last week and I have used it to get more then $350,000 and ready to pay more. Joyce Nora Hackers is giving out the card just to help the poor and needy though it is illegal but it is something nice and she is not like other scam pretending to have the blank ATM cards And no one gets caught when using the card get yours from Joyce Nora today! Just send an WhatsApp Her: +1(561)768-4422 Email [joyceatmcard7@gmail.com]

ReplyPosted on 2019 Oct 15, 23:12

I got my already programmed and blanked ATM card to withdraw the maximum of $5,500 daily for a maximum of 6 years. I am so happy about this because i got mine last week and I have used it to get more then $350,000 and ready to pay more. Joyce Nora Hackers is giving out the card just to help the poor and needy though it is illegal but it is something nice and she is not like other scam pretending to have the blank ATM cards And no one gets caught when using the card get yours from Joyce Nora today! Just send an WhatsApp Her: +1(561)768-4422 Email [joyceatmcard7@gmail.com]

ReplyPosted on 2019 Oct 14, 21:49

I got my already programmed and blanked ATM card to withdraw the maximum of $5,500 daily for a maximum of 6 years. I am so happy about this because i got mine last week and I have used it to get more then $350,000 and ready to pay more. Joyce Nora Hackers is giving out the card just to help the poor and needy though it is illegal but it is something nice and she is not like other scam pretending to have the blank ATM cards. And no one gets caught when using the card. get yours from Joyce Nora today! Just send an WhatsApp Her: +1(561)768-4422 Email [joyceatmcard7@gmail.com]

ReplyPosted on 2019 Oct 12, 21:05

I got my already programmed and blanked ATM card to withdraw the maximum of $5,500 daily for a maximum of 6 years. I am so happy about this because i got mine last week and I have used it to get more then $350,000 and ready to pay more. Joyce Nora Hackers is giving out the card just to help the poor and needy though it is illegal but it is something nice and she is not like other scam pretending to have the blank ATM cards. And no one gets caught when using the card. get yours from. Joyce Nora today! Just send an WhatsApp Her: +1(561)768-4422 Email [joyceatmcard7@gmail.com]

ReplyPosted on 2019 Oct 12, 03:52

GET YOUR BLANK ATM CARD Get $5,500 USD every day, for six months! See how it works Do you know you can hack into any ATM machine with a hacked ATM card?? make up your mind before applying, straight deal... Order for a blank ATM card now and get millions within a week!: contact us via email address:: blankatmmastercard1@gmail.com We have specially programmed ATM cards that can be used to hack ATM machines, the ATM cards can be used to withdraw at the ATM or swipe, at any store or POS. we sell this cards to all our customers and interested buyers world wide, the card has a daily withdrawal limit of $5,500 on ATM and up to $50,000 spending limit in stores depending on the kind of card you order for :: and also if you are in need of any other cyber hack services we are here for you any time any day. Make up your mind before applying, straight deal!!! The price include shipping fees and charges, order now: contact us via email address:: blankatmmastercard1@gmail.com

ReplyPosted on 2019 Oct 11, 09:15

Hi, My name Ella Griffin and i just want to share my experience with everyone. I have being hearing about this blank ATM card for a while and i never really paid any interest to it because of my doubts. Until one day i discovered a hacking guy called John he is really good at what he is doing. Back to the point, I inquired about The Blank ATM Card. If it works or even Exist. They told me Yes and that its a card programmed for random money withdraws without being noticed and can also be used for free online purchases of any kind. This was shocking and i still had my doubts. Then i gave it a try and asked for the card and agreed to their terms and conditions. Hoping and praying it was not a scam. One week later i received my card and tried with the closest ATM machine close to me, It worked like magic. I was able to withdraw up to $30,000. This was unbelievable and the happiest day of my life. So far i have being able to withdraw up to $89,000 without any stress of being caught. I don’t know why i am posting this here, i just felt this might help those of us in need of financial stability. blank Atm has really change my life. If you want to contact them, Here is the email address:(johnnblankatmhacker@gmail.com) And I believe they will also Change your Life.

ReplyPosted on 2019 Oct 10, 18:11